Battery recycling: The missing link in India’s EV supply chain?

- Kalyan Chatterjee

- Oct 2, 2024

- 9 min read

Updated: Nov 9, 2025

As India pushes for electric vehicles to meet climate goals, critical mineral shortages could be addressed through battery recycling, but the largely informal sector lacks regulation, capacity, and government support.

In 2021, at Glasgow Climate Summit, Indian Prime Minister Narendra Modi announced India’s goal of achieving net-zero by 2070. As a consequence, the country has spurred into action to quicken its pace on putting EVs on the road. It has resolved that by 2030 at least 30% of passenger cars, 70 % of commercial vehicles and 80% of two- and three-wheelers on its roads would be electric.

However, this ambitious plan faces a rather crucial roadblock. India does not produce many of the critical minerals for manufacturing batteries for EVs like lithium, cobalt and nickel. Further, the scale of Chinese domination in EV manufacturing and possession of components required for the manufacturing makes India look like an insignificant player in the global EV supply chain.

In the face of these challenges, recycling the large amounts of these critical minerals accumulating in massive e-waste that the country generates presents itself as a viable solution. There are some questions, however, that come up. How much of these critical minerals can India procure through recycling? How well regulated is the recycling sector at the moment? Does India have the technological capacity to recycle these minerals into top quality raw materials, say battery grade lithium? CarbonCopy delves into all these questions here.

EV is here to stay

After initial hesitation, dominant global wisdom has once again zeroed in on electric traction to power the transport sector. Electric vehicles or EVs were tried out on American roads in the closing years of the last century, but despite all round satisfaction they were given a quiet burial in 2003. Oil was still king and it was feared that EVs would destabilise the petroleum-based internal combustion engine-dominated auto industry. Now, of course, petroleum, a fossil fuel, has been identified as the third-biggest contributor to global warming after power and industry. EVs, therefore, are strongly back in favour as they are believed to hold the key to checking global warming and meet climate goals.

Although action to limit carbon emissions has accelerated and acquired urgency after the 2015 Paris Climate Summit, China had already emerged as the world leader both in the manufacture of electric vehicles and the components that go into their making by then. It is not surprising, therefore, that more than half of all EVs run on Chinese roads.

Compared to China, India has been a slow starter, framing serious policy only in 2015 to manufacture with the introduction of a scheme called Faster Adoption and Manufacturing of (Hybrid and) Electric Vehicles with the acronym FAME with an investment of ₹895 crore. But even so, the results produced over the next four years were disappointing, to say the least. By 2019, it had managed to put only 28,000 two-wheelers and 143,000 three wheelers and only 2,377 cars on the road. In 2019, the government initiated the second phase in FAME 2 for a period of three years with an outlay of ₹10,000 crore, over ten times the outlay of the first phase. This time around, the results were more encouraging with two-wheeler sales jumping to over 250,000, three-wheelers to 172,000 and four-wheelers to over 18,000 by 21-22. But these were still well short of expectations. The following two years, the spike was even more impressive with two-wheeler sales going up to just under a million and four-wheelers to about 90,000 by 23-24. The total number of EV four-wheelers (with much larger batteries than two- and three-wheelers) on the roads in India is just over 200,000, which is a very small fraction of more than four million two-wheelers sold in 2023-24.

The government is considering a number of options to overcome this bottleneck, but most of them will take a while to mature. For the moment, the only viable option that can ensure a steady supply chain of these materials seems to be recycling the large amounts of these critical minerals that have accumulated in the large numbers of LiB-powered consumer electronics devices over the years such as discarded mobile phones, laptops and tablets.

The importance of circularity was emphasised earlier this month in a resolution on sustainability called ‘Pact for the Future’, which was adopted by the UN to achieve sustainable production and consumption. This comes about 50 days before COP 29 Climate Summit scheduled to open in Baku, Azerbaijan in November. In early 2025, parties are expected to submit updated Nationally Determined Contributions (NDC 3.0) or what has been called the ‘third generation national climate plans.’. It is clear that timelines are tight, but the government has delayed the announcement of FAME 3 (faster adoption and manufacturing of Electric and Hybrid vehicles) as a sequel to FAME 2 announced in 2019. The term of FAME 2 ended in 2022, but in the absence of the next phase, a new Electric Mobility Promotion Scheme (EMPS) was announced in April 2024 and is expected to continue till FAME 3 is ready.

Critical minerals import surge

The biggest obstacle to the manufacture of EVs in India was that they did not produce some of the crucial ingredients, including metals like lithium and cobalt, which are the heart and soul of EVs. Naturally, India turned to imports to implement FAME. Today, the country imports more than 95% of its LIB batteries. – 63% from China and the rest from Hong Kong (22%), Vietnam (9%) and the United States (2%), according to a study carried out by PricewaterhouseCoopers for NITI Aayog and published in September, 2020. In 2023, India’s battery import bill was $2.1 billion.

But the post-Covid supply chain disruptions have driven home the lesson that procurement of critical ingredients could not be left to the vagaries of an uncertain global supply chain. So, the search in India branched off in two other directions – exploration and setting up joint ventures in countries that had large deposits of these metals. Explorations have unearthed large deposits of lithium, while at the same time, a new consortium of three state-owned Indian mining companies, formed to target overseas deposits, has struck deals with some South American countries and Australia. But both are in preliminary stages and may even take well up to a decade to mature. Clearly, India can’t afford to wait that long to meet even its 2030 climate goals.

Recycling to secure supply

The only secure and immediate supply of lithium, cobalt and other rare metals, therefore can be obtained by recycling the considerable stocks of LIB batteries built up over the years in such consumer electronic powered devices like laptops, mobile phones and tablets imported for the last couple of decades. Critical minerals could be recovered from used lithium-ion batteries through a process that has come to be described as urban mining. A recent Rocky Mountain Institute (RMI) report says that circularity will “kickstart a perpetual motion machine.”

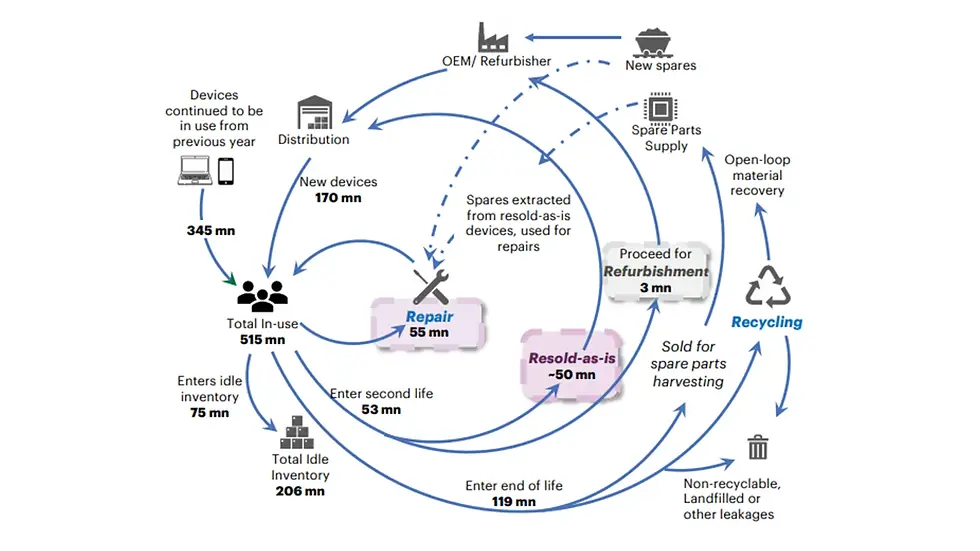

A 2022 NITI Aayog Report has said that the consumer electronics sector currently uses 51% of all LIBs. This is not surprising as the number of smartphones has grown exponentially from 14.5 million in 2011 to 150 million in 2020, according to the report. The Indian Cellular & Electronics Association (ICEA) estimates that the total number of smartphones and laptops in the country in 2021 was more than half-a-billion, to which 170 million are added every year. Of these, 119 million enter the recycling and refurbishing streams every year. Each smartphone, for example, contains about 5% cobalt, 0.35% lithium and 1.6% nickel, according to ICEA data. The estimated cumulative stock of LIBs was 15 GWh in 2020.

If India is to achieve 30% of EV penetration by 2030, it can need as much as 800 GWh of batteries, according to a report by consulting firm Arthur D Little.

Comments